Brasil · May 2026

Taxes in Brazil for Expats 2026

Receita Federal and CPF for foreigners, progressive IRPF income tax, the new R$5,000 exemption, worldwide income, Carnê-Leão, INSS, and tax residency rules — with official sources

Brazil has a complex, federally administered tax system overseen by the Receita Federal do Brasil (RFB). For foreigners, the key question is whether they are Brazilian tax residents: if so, their worldwide income is subject to the progressive IRPF (Imposto de Renda Pessoa Física) at rates from 7.5% to 27.5%. Tax residency arises automatically for permanent-visa and employed temporary-visa holders, and after more than 183 days of physical presence within any 12-month period for everyone else.

Brazil operates on self-assessment: residents calculate and declare their own income through Receita Federal systems. A CPF (Cadastro de Pessoas Físicas) — the individual taxpayer ID — is required for almost any economic activity: opening a bank account, signing a lease, buying property, or filing a return. Any foreigner can obtain a CPF, and it does not by itself grant residence or work rights.

This guide reflects the IRPF rules in force for 2026, including Lei 15.270/2025, which from 1 January 2026 fully exempts monthly income up to R$5,000 and phases out partial relief up to R$7,350. Brazilian tax law changes frequently — always verify current figures at gov.br/receitafederal and consult a licensed contador (accountant).

This page is general information only and is not tax, legal, or financial advice. For a cross-country comparison with Argentina, Mexico, Colombia, Panama, and Uruguay — including filing deadlines, tax ID glossary, and territorial vs worldwide regimes — see the Latin America Expat Tax Calendar guide (/en/guides/latam-expat-tax-calendar).

Key Figures

| Tax authority | Receita Federal | Receita Federal do Brasil — gov.br/receitafederal |

| Income tax (IRPF) | 7.5%–27.5% | Progressive scale; worldwide income for tax residents |

| Exemption from 2026 | Up to R$5,000/month | Full IRPF exemption; partial relief up to R$7,350 (Lei 15.270/2025) |

| Tax residency threshold | > 183 days / 12 months | Or immediately for permanent / employed temporary visas |

| Taxpayer ID | CPF | Cadastro de Pessoas Físicas; available to any foreigner |

| Capital gains | 15%–22.5% | Progressive by gain size (Lei 13.259/2016) |

| INSS (employee) | 7.5%–14% | 2026 ceiling R$8,475.55/month |

| Annual declaration (DIRPF) | March–May | IRPF 2026 window: 23 Mar – 29 May 2026 |

Tax System Overview

Brazil divides taxes across three levels of government: federal (IRPF income tax, IPI, contributions), state (ICMS sales tax, IPVA vehicle tax), and municipal (ISS service tax, IPTU urban property tax). For individuals, the most relevant is IRPF, administered by the Receita Federal do Brasil.

For individuals, IRPF is a progressive tax on total income. Brazilian tax residents must declare worldwide income; non-residents pay only on Brazilian-source income, generally at flat withholding rates with no deductions allowed (25% on employment and services, 15% on rents and most other income).

Brazil has double-taxation treaties with around 37 countries, including Spain, Portugal, Argentina, Canada, China, France, Italy, and Japan. Brazil has no formal treaty with the United States, but officially recognises reciprocity of tax treatment with the US, the UK, and Germany, allowing a foreign tax credit on the same income.

| Tax | Base | Rate |

|---|---|---|

| IRPF (income tax) | Worldwide income (residents); Brazilian-source income (non-residents) | 7.5%–27.5% (progressive) |

| INSS (social security) | Salary up to the ceiling | 7.5%–14% (progressive) |

| Capital gains (ganho de capital) | Gain on sale of assets | 15%–22.5% |

| IPTU (urban property tax) | Cadastral value of real estate | ~0.3–1.5% per year (municipal) |

Tax Residency in Brazil

Tax residency in Brazil depends on visa type and physical presence. A holder of a permanent visa becomes a tax resident from the date of entry. A holder of a temporary visa with a Brazilian employment contract also becomes a resident from the date of entry. A holder of a temporary visa without an employment contract becomes a resident only after completing 183 days of physical presence in Brazil — consecutive or not — within any 12-month period.

The 183-day rule counts days of actual physical presence in Brazil within a rolling 12-month window. During the first 183 days the person remains a non-resident; once the threshold is crossed they are treated as a tax resident for income-tax purposes from that point. Tax residency is independent of immigration status: it is the day count and visa category that matter.

Ceasing tax residency requires filing a Comunicação de Saída Definitiva do País (notice of definitive departure) and the corresponding final declaration with the Receita Federal; otherwise Brazil may continue to treat you as a resident with worldwide-income obligations.

Digital nomads who spend fewer than 183 days as tourists generally do not become tax residents. Those who exceed 183 days, or who arrive on a permanent or employed temporary visa, become residents and must report worldwide income — a consultation with a Brazilian contador is strongly advised.

IRPF — Income Tax

IRPF (Imposto de Renda Pessoa Física) is the main direct tax on individuals in Brazil. For resident individuals, the statutory progressive rates are 7.5%, 15%, 22.5%, and 27.5%, applied band by band using a "parcela a deduzir" (amount to deduct) to compute the monthly tax.

From 1 January 2026, Lei 15.270/2025 fully exempts monthly income up to R$5,000 (R$60,000 per year), delivered as an IRPF reduction of up to R$312.89 per month. A partial reduction applies for monthly income from R$5,000.01 to R$7,350.00, declining to zero at R$7,350. The underlying 7.5%–27.5% rate structure remains; the reform layers a reduction on top of it.

Permitted deductions for residents include dependents, education expenses (capped), medical expenses (uncapped with valid receipts), and official social-security (INSS) contributions. Taxpayers may instead choose the simplified deduction (desconto simplificado) in place of itemising. This is general information only — confirm your eligibility with a contador.

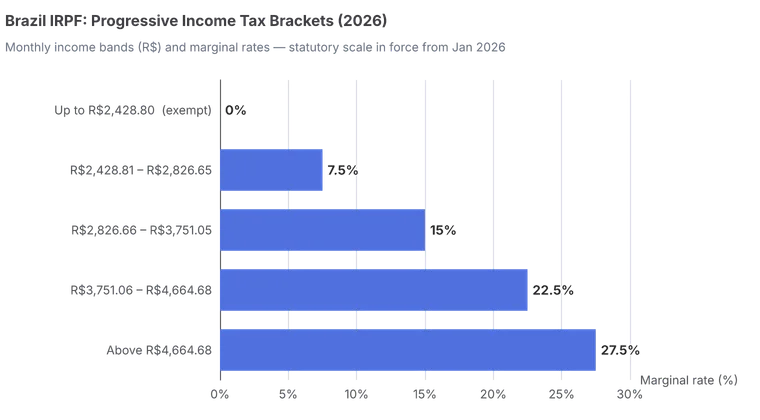

Progressive IRPF scale for individuals (2026)

The table below shows the statutory monthly brackets in force in 2026. Rates apply band by band; the "amount to deduct" simplifies the per-bracket calculation. From January 2026 a separate reduction fully offsets tax for monthly income up to R$5,000.

| Monthly income (R$) | Rate | Amount to deduct (R$) |

|---|---|---|

| Up to 2,428.80 | Exempt (0%) | — |

| 2,428.81 – 2,826.65 | 7.5% | 182.16 |

| 2,826.66 – 3,751.05 | 15.0% | 394.16 |

| 3,751.06 – 4,664.68 | 22.5% | 675.49 |

| Above 4,664.68 | 27.5% | 908.73 |

CPF for Foreigners

The CPF (Cadastro de Pessoas Físicas) is Brazil's individual taxpayer identification number — roughly equivalent to a US Social Security number. It is required to open a bank account, sign a rental or service contract, buy property, get a phone line, and to file any tax return. Almost no formal economic activity is possible without one.

Any foreigner can obtain a CPF — tourists, students, remote workers, investors, and spouses included. Crucially, the CPF is purely an identification and tax number: it does not grant residence or the right to work in Brazil.

How to get a CPF: inside Brazil, apply at a Receita Federal service point or at a partner institution (Banco do Brasil, Caixa, Correios, or a notary/cartório). From abroad, apply at a Brazilian consulate via the e-Consular system or through the Receita Federal online portal. At Receita offices and consulates the number is usually issued immediately; partner locations may take a few days.

Foreign Income & Carnê-Leão

Brazilian tax residents are taxed on worldwide income: foreign salary, foreign rent, and foreign investment returns are all reportable. Where foreign-source income is not subject to Brazilian withholding, it is collected through the Carnê-Leão — a monthly self-assessment using the same progressive IRPF table.

The Carnê-Leão (defined by the Receita Federal as the monthly tax on income received by a Brazilian resident from another individual or from abroad) applies to the self-employed, landlords renting to individuals, freelancers, and anyone receiving foreign-source income. This makes it directly relevant to remote workers and digital nomads who become tax residents.

Carnê-Leão payments are due by the last business day of the month following receipt of the income, and are reconciled in the annual DIRPF declaration. Income paid in foreign currency is converted using the official exchange rate. For US persons, the absence of a Brazil–US treaty is mitigated by reciprocity, which allows tax paid in one country to be credited against tax on the same income in the other.

Capital Gains & INSS

Capital gains (ganho de capital) on the sale of assets by individuals are taxed at progressive rates under Lei 13.259/2016: 15% on gains up to R$5 million, 17.5% from R$5 million to R$10 million, 20% from R$10 million to R$30 million, and 22.5% above R$30 million. An exemption may apply to the sale of a residential property when 100% of the proceeds are reinvested in another Brazilian residential property within 180 days.

INSS (Instituto Nacional do Seguro Social) is the social-security contribution withheld from employees, applied band by band at 7.5%, 9%, 12%, and 14%. For 2026 the contribution ceiling is R$8,475.55 per month, so the maximum monthly employee contribution is roughly 14% of that ceiling. Self-employed contributors and company partners follow separate rules.

Foreigners working under a Brazilian employment contract have INSS withheld automatically. Those who are self-employed or receive foreign income should clarify their INSS position — Brazil has totalisation (social-security) agreements with several countries that can prevent double contributions.

| Salary band (R$) | Rate | Amount to deduct (R$) |

|---|---|---|

| Up to 1,621.00 | 7.5% | — |

| 1,621.01 – 2,902.84 | 9.0% | 24.32 |

| 2,902.85 – 4,354.27 | 12.0% | 111.40 |

| 4,354.28 – 8,475.55 | 14.0% | 198.49 |

Annual DIRPF Declaration

Brazilian tax residents file the annual Declaração de Ajuste Anual (DIRPF) with the Receita Federal, typically between mid-March and the end of May. For the 2026 cycle (covering 2025 income), the filing window runs from 23 March to 29 May 2026. Returns are filed through the Receita Federal program (PGD) or the "Meu Imposto de Renda" online service.

Filing is mandatory above certain thresholds — for example, taxable income above R$35,584 in the IRPF 2026 cycle, along with thresholds for exempt income, securities trades, asset holdings, and rural income. Taxpayers below the thresholds may still file voluntarily, often to claim a refund of tax withheld at source.

Late filing triggers a fine of 1% per month (or fraction) of the tax due, with a minimum of R$165.74 and a maximum of 20% of the tax owed. The minimum fine applies even when no tax is due or a refund is expected, and Selic-rate interest accrues on amounts left unpaid. Persistent non-compliance can block the CPF and cause banking difficulties.

FAQ

Do I have to pay Brazilian taxes while working remotely as a tourist?

If you spend fewer than 183 days in Brazil within a 12-month period and work for a foreign employer, generally no Brazilian income tax applies. However, once you exceed 183 days you become a tax resident and must report worldwide income, paying foreign-source income through the Carnê-Leão. The line can be blurred, so a consultation with a contador is recommended before relying on the threshold.

How do I get a CPF as a foreigner?

Any foreigner can obtain a CPF. Inside Brazil, apply at a Receita Federal office or a partner institution such as Banco do Brasil, Caixa, Correios, or a notary. From abroad, apply at a Brazilian consulate via the e-Consular system or through the Receita Federal portal. The CPF is an identification and tax number only — it does not grant residence or work rights, and it is usually issued immediately at official offices.

What changed with the 2026 income tax exemption?

From 1 January 2026, Lei 15.270/2025 fully exempts monthly income up to R$5,000 (R$60,000 per year) from IRPF, through a reduction of up to R$312.89 per month. A partial reduction applies for monthly income between R$5,000.01 and R$7,350, declining to zero at R$7,350. The underlying 7.5%–27.5% rate structure stays the same; the reform simply adds a reduction on top of it.

Does Brazil have a tax treaty with the United States?

No, Brazil and the United States do not have a formal double-taxation treaty. However, Brazil officially recognises reciprocity of tax treatment with the US (as well as the UK and Germany), which allows tax paid in one country to be credited against tax on the same income in the other. US persons should still file in both countries and coordinate their foreign tax credits to avoid double taxation.

What is the Carnê-Leão and do freelancers need it?

The Carnê-Leão is a monthly mandatory self-assessment of IRPF on income received by a Brazilian resident from another individual or from abroad, where no Brazilian withholding applies. It covers the self-employed, landlords renting to individuals, freelancers, and anyone with foreign-source income. Payment is due by the last business day of the following month, using the same progressive IRPF table, and is reconciled in the annual DIRPF.

What happens if I file my annual declaration late?

Late filing of the DIRPF triggers a fine of 1% per month (or fraction) of the tax due, with a minimum of R$165.74 and a maximum of 20% of the tax owed. The minimum fine applies even if no tax is due or a refund is expected. Selic-rate interest accrues on any unpaid balance, and persistent non-compliance can lead to the CPF being blocked and to banking difficulties.

How is capital gains tax calculated in Brazil?

Capital gains on the sale of assets by individuals are taxed progressively under Lei 13.259/2016: 15% on gains up to R$5 million, 17.5% up to R$10 million, 20% up to R$30 million, and 22.5% above R$30 million. The sale of a residential property can be exempt if 100% of the proceeds are reinvested in another Brazilian residential property within 180 days. This is general information and not a substitute for professional advice.

Do I need to declare foreign bank accounts and income in Brazil?

Brazilian tax residents must report all worldwide income in the DIRPF, including foreign salary, foreign rent, and investment returns from abroad. Foreign assets and balances above certain thresholds must also be declared in the annual return, and a separate central-bank declaration (CBE) applies to larger holdings. Brazil exchanges financial information with other tax authorities under the OECD Common Reporting Standard.

See also

Guide

Latin America Expat Tax Calendar

Six-country comparison of tax regimes, filing deadlines, and tax ID glossary.

Sources

| Source | Description | Accessed |

|---|---|---|

| Receita Federal do Brasil | Brazil's federal tax authority — CPF, IRPF, DIRPF, Carnê-Leão | May 2026 |

| Receita Federal — Carnê-Leão | Official guidance on monthly Carnê-Leão for foreign-source income | May 2026 |

| Receita Federal — IR reduction from 2026 | Official orientation on the R$5,000 monthly IRPF exemption from Jan 2026 | May 2026 |

| Lei nº 15.270/2025 | Statute raising the IRPF exemption to R$5,000/month from 2026 | May 2026 |

| gov.br — Apurar ganho de capital | Official service page for capital gains tax calculation | May 2026 |

| PwC — Brazil Individual Tax Summary | Residency, income tax, capital gains, and treaty overview | May 2026 |

| INSS — Instituto Nacional do Seguro Social | Social-security contribution tables, ceilings, and rules | May 2026 |

Tax rates and thresholds are updated frequently, and 2026 figures reflect recent reforms. This guide is informational only and does not constitute tax, legal, or financial advice. Consult a licensed Brazilian contador before making tax-related decisions.